The Asymmetry Nobody Talks About

China's capital markets have spent a decade opening their financial channels. Stock Connect, the QFII and RQFII expansion, MSCI A-share inclusion — each has incrementally lowered the barrier for foreign money to enter. Yet foreign institutional ownership of A-shares remains structurally depressed relative to China's weight in global GDP and corporate earnings.

The standard explanations — VIE risk, regulatory unpredictability, currency controls — are real but incomplete. The underappreciated constraint is information liquidity: not the absence of information, but the absence of information in a form that global capital can consume efficiently.

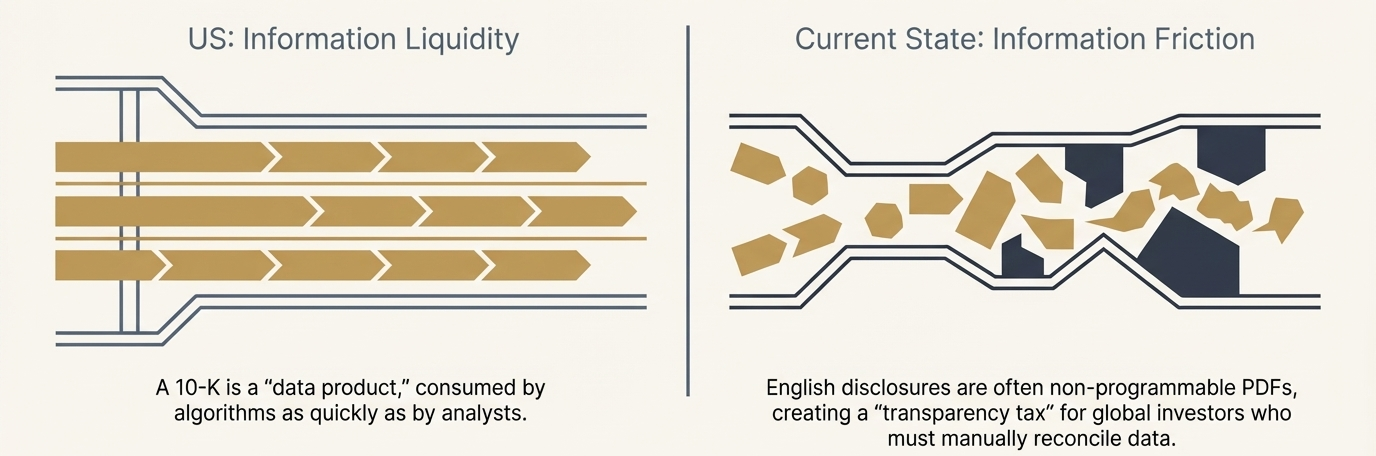

Fig. 1 — Capital channels are open; information channels are not

A US 10-K is not merely a legal document. It is a data product — structured in XBRL, centrally hosted on EDGAR, consumed simultaneously by algorithms and analysts within minutes of filing. A comparable Chinese annual report arrives as a Mandarin-primary PDF, hosted across three separate exchange portals (SSE, SZSE, BSE), with ad hoc announcements in variable formats that resist automated parsing.

The global investor who wants to analyse Kweichow Moutai with the same efficiency as Apple faces a transparency tax measured not in fees but in time, translation cost, and interpretive uncertainty.

Quantifying the Gap

| Dimension | US — SEC Standard | China — 2026 State | Proposed Solution |

|---|---|---|---|

| Language | English — global default | Mandarin primary / English partial | Dual-language mandatory — CSI 300 |

| Data Format | XBRL / Inline XBRL | XBRL domestic / PDF global | Global-standard JSON/XBRL API |

| Filing Types | 10-K, 10-Q, 8-K (standardised) | Annual, Interim, Ad Hoc (variable) | Standardised event-driven codes |

| Access | Centralised — EDGAR | Fragmented — SSE / SZSE / BSE | Unified National Disclosure Portal |

Each row represents not a cosmetic difference but a genuine friction cost borne by every foreign asset manager, quant fund, and data vendor attempting systematic analysis of Chinese equities. Aggregated across the global institutional universe, this friction constitutes a de facto discount on Chinese listed companies — unrelated to their underlying economics.

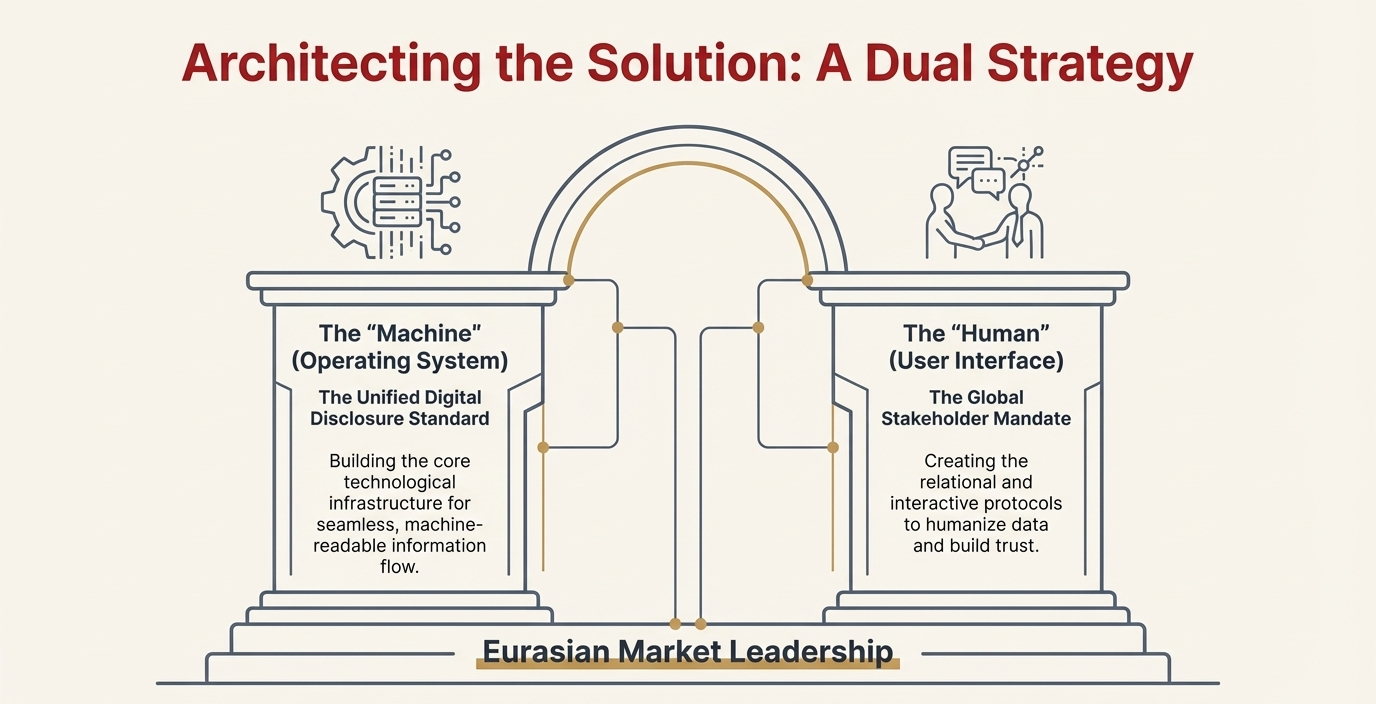

A Two-Pillar Solution

The proposal frames the solution as an operating system — infrastructure that runs beneath the market, enabling everything above it to function more efficiently. It has two distinct but complementary components.

The Machine — Unified Digital Disclosure Standard

A bilingual XBRL taxonomy where a single tag maps simultaneously to Mandarin and English data points. Standardised event codes replacing variable ad hoc announcements. A centralised China-EDGAR portal with programmable API access.

The Interface — Global Stakeholder Mandate

Mandatory Quarterly Interactive Briefings with substantive English Q&A. A Strategic Global IR Director at CSI 300 companies as a trust proxy. A CSRC-backed calendar of digital roadshows and investor days.

Fig. 2 — The dual-pillar architecture: technical infrastructure paired with human engagement protocols

These two pillars have fundamentally different implementation profiles. The UDDS is a technical infrastructure problem — solvable with regulatory mandate and modest investment, analogous to the SEC's XBRL rollout between 2009 and 2011. The Global Stakeholder Mandate requires behavioural change at board and management level. The sequencing implication is clear: build the machine first; mandate the interface second.

The ESG Window — A Trojan Horse with Impeccable Timing

Starting this month, over 400 large-cap Chinese companies are required to publish their first mandatory Sustainability Reports under CSRC guidelines. This creates a window the proposal calls the "Trojan Horse" opportunity.

Global patient capital — the most sought-after investor class — is heavily ESG-driven. Mandating new bilingual digital standards for ESG data first will build the infrastructure and precedent needed to extend those standards across all financial reporting.

ESG reporting is the ideal pilot because it is new (no legacy compliance infrastructure to disrupt), globally scrutinised, and politically palatable — aligning with China's own dual-carbon commitments. A company that files a machine-readable, dual-language sustainability report in May 2026 has already built most of the infrastructure needed for a machine-readable annual report in 2027.

A Pragmatic Roadmap

The pilot begins with the CSI 100 — the 100 largest and most institutionally resourced listed companies — and proceeds in two phases within a single calendar year, with full extension thereafter.

Digital OS Implementation

CSI 100 companies file FY2025 Annual Reports using full Bilingual XBRL standard. SSE and SZSE launch the English-language "Global Gateway" portal aggregating all CSI 100 filings in machine-readable format.

Interactive Rollout

Mandatory English-language Quarterly Interactive Briefings begin for all CSI 100 firms. CSRC establishes an Institutional Feedback Loop with top global asset managers to measure information friction reduction.

Full CSI 300 Extension

Halo effect from CSI 100 success drives voluntary adoption across the broader listed universe. Standard embedded in 15th Five-Year Plan metrics. Eurasian disclosure framework established.

Beyond Disclosure: The Debt-to-Equity Transition

The proposal situates the information infrastructure argument within China's broader macroeconomic challenge: a corporate sector historically over-reliant on debt financing, now navigating a deleveraging imperative under the 15th Five-Year Plan. The connection is direct — equity is a more efficient, risk-absorbing form of capital, but only when markets are sufficiently transparent to attract long-term institutional investors at scale.

Fundamentally, equity markets alleviate the complexities and strains of debt markets. The disclosure standard is not merely a transparency reform — it is a capital structure reform delivered in infrastructure form.

What This Is Not Claiming

Intellectual honesty requires stating the limits. Information friction is one constraint on China's equity market valuation — not the only one. VIE structural risk, extraterritorial enforcement uncertainty, currency non-convertibility, and periodic regulatory intervention are real and persistent. A disclosure standard does not eliminate these. What it removes is the friction that is most directly addressable by regulatory action — and within China's unilateral control to fix without external negotiation or geopolitical concessions.

The CSI 100 pilot structure is partly designed to navigate around the most sensitive constraint: genuine transparency requirements for state-owned enterprises will encounter structural resistance where information control is an active policy tool. Beginning with less sensitive sectors demonstrates value first, and builds the political case for broader extension.